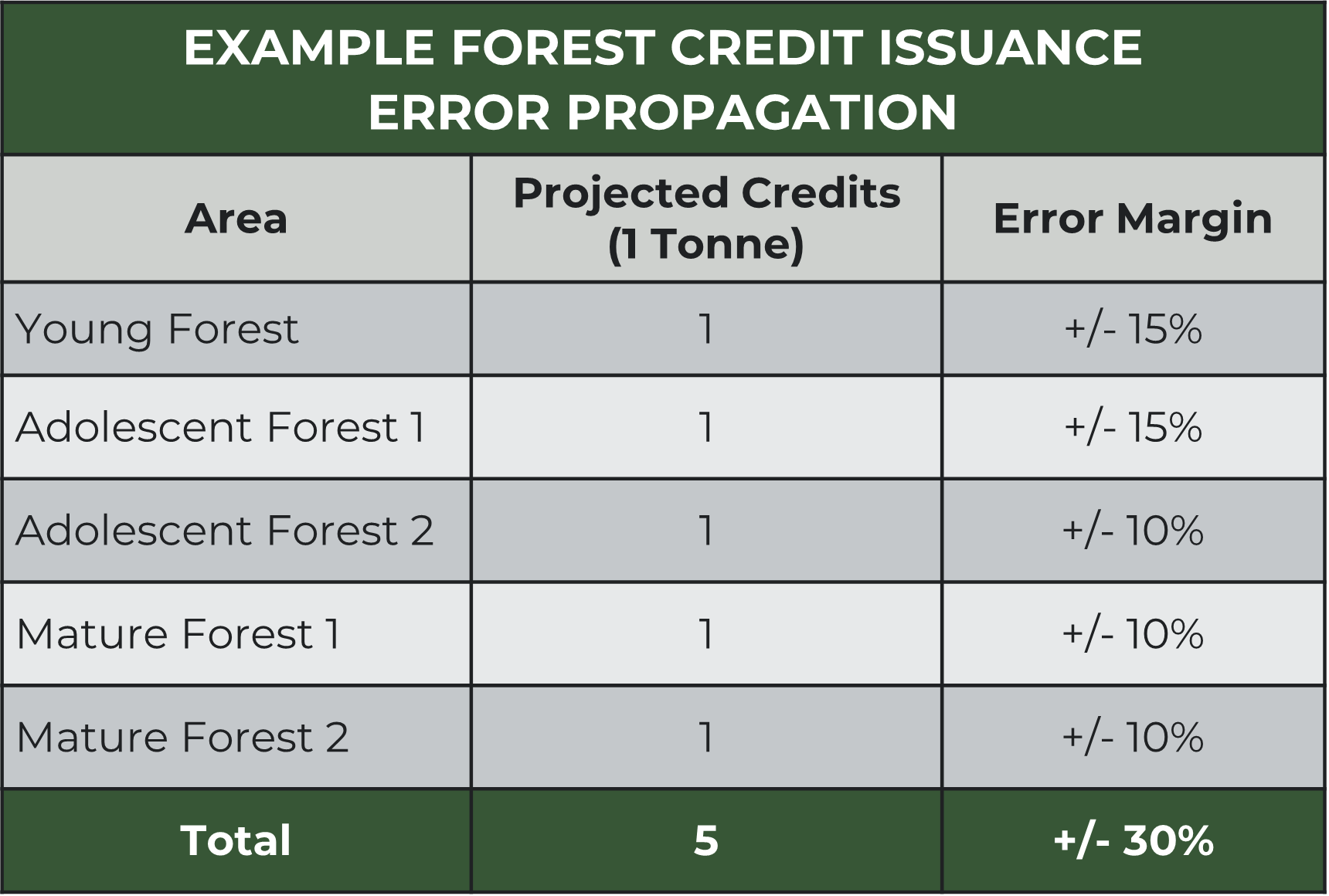

Insights

How carbon measurement uncertainty is impeding carbon market viability

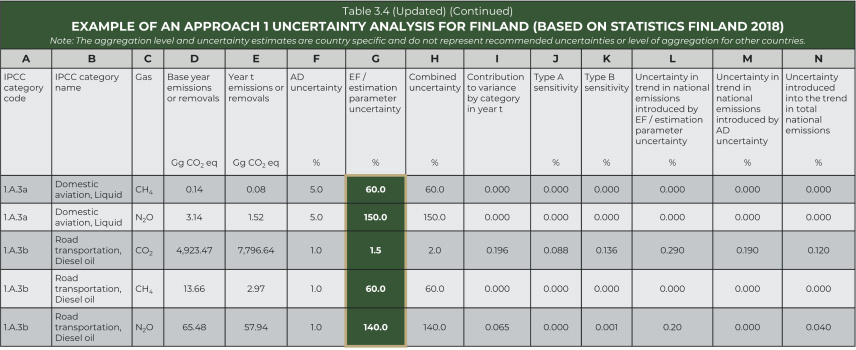

Example Emissions Factor Uncertainty from the 2019 Refinement to the 2006 IPCC Guidelines for National Greenhouse Inventorieswith 1.5%-150% emissions factor uncertainty highlighted.